The Blog

rolling-reserve-merchant-account-the-complete-guide-for-high-risk-b2b-businesses

For businesses operating in high-risk industries, securing and maintaining a stable merchant account is often more challenging than generating sales. One of the most common — and misunderstood — mechanisms used by payment providers is the rolling reserve merchant account.

This guide explains what a rolling reserve is, why it exists, how it affects cash flow, which industries require it, and how companies can reduce or negotiate it. More importantly, it shows how specialized providers like NextGen Payment manage rolling reserves transparently to protect both merchants and payment ecosystems.

If you operate in industries such as online casinos, betting, trading, CBD, subscriptions, or international B2B, understanding rolling reserves is critical to making informed financial decisions.

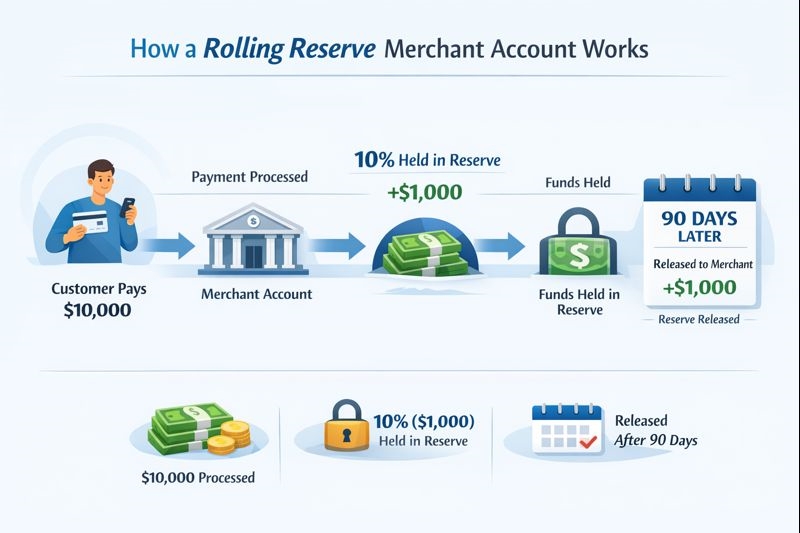

A rolling reserve merchant account is a payment processing arrangement where a percentage of each transaction is temporarily withheld by the payment provider to cover potential risks such as chargebacks, fraud, refunds, or regulatory disputes.

Instead of blocking all funds upfront, the reserve “rolls” over time. For example, if a provider applies a 10% rolling reserve for 90 days, 10% of each day’s processed volume is held and then released after 90 days — assuming no major issues occur.

A rolling reserve is a risk-management buffer that protects payment processors and acquiring banks while allowing high-risk merchants to continue accepting payments.

Understanding the difference between reserve models is essential:

A fixed percentage (e.g., 5–15%) of each transaction is held for a defined period (usually 90–180 days) and released gradually.

A lump sum is required before processing begins. This is common for very high-risk or new merchants with limited history.

Funds are held until a predefined amount is reached (for example, €50,000), after which no additional reserves are collected.

Among these, rolling reserves are the most balanced solution for ongoing high-risk B2B operations.

Rolling reserves are not penalties. They exist because payment providers operate in a highly regulated environment with financial, legal, and reputational exposure.

High-risk industries statistically experience:

Card networks like Visa and Mastercard impose strict monitoring programs. If thresholds are exceeded, providers face fines, audits, or even termination.

Industries such as:

often deliver products or services weeks or months after payment. If delivery fails, disputes arise long after funds have been settled.

Acquiring banks require payment processors to:

Rolling reserves are often mandated by banks, not optional decisions by payment platforms.

For decision-makers, cash flow impact is the most important factor.

Result:

For B2B companies:

For subscription models:

The key is predictability, not avoidance.

Certain industries are classified as high-risk due to structural characteristics, not poor business practices.

High transaction volumes, regulatory scrutiny, fraud exposure.

Chargeback spikes, jurisdictional restrictions, AML concerns.

Market volatility, dispute complexity, regulatory variation.

High fraud rates, card network sensitivity.

Regulatory ambiguity, refund disputes, compliance challenges.

Future delivery risk, cancellations, seasonal volatility.

Recurring billing disputes, churn-related chargebacks.

Mainstream providers prioritize low-risk scalability. When risk increases:

Specialized providers like NextGen Payment exist specifically to prevent this outcome.

Rolling reserves are not fixed forever. They can often be optimized.

Maintaining ratios well below card network thresholds is essential.

Real-time monitoring, velocity checks, device fingerprinting, and behavioral analysis significantly reduce risk perception.

Consistent month-over-month volumes indicate operational maturity.

Clear terms, refund policies, and customer communication reduce disputes.

This is where NextGen Payment adds strategic value:

For many businesses, the choice is not between no reserve or reserve — it is between a rolling reserve or no merchant account at all.

NextGen Payment approaches rolling reserves as a collaborative financial strategy, not a hidden restriction.

Merchants know:

No unexpected freezes or unexplained deductions.

Reserves are structured to align with:

Dedicated advisors:

Many merchants experience:

This long-term approach differentiates NextGen Payment from transactional providers.

Typically 90 to 180 days, depending on industry, risk level, and processing history.

Yes. Funds are released according to the agreed schedule, provided there are no unresolved disputes.

Yes. Improved chargeback ratios, fraud prevention, and stable volume often lead to renegotiation.

Not always, but most high-risk industries require some form of reserve at least initially.

Absolutely — especially when working with specialized providers like NextGen Payment.

A rolling reserve merchant account is not a barrier to growth — it is a mechanism that enables high-risk B2B businesses to operate securely, compliantly, and at scale.

For companies in regulated or high-risk industries, the real risk lies in choosing providers that do not understand their business model. By offering transparency, predictability, and strategic optimization, NextGen Payment transforms rolling reserves from a limitation into a foundation for sustainable growth.

When stability matters more than shortcuts, rolling reserves become a strategic advantage — not a compromise.

.png)